How to take Bigger loan with Pledging or Show cash | Overcoming TDSR

In this video, we are going to share with you how to take a bigger loan, using the Pledging or Show-Cash method in order to buy your dream home.

📌TDSR Impact

Before we talk about pledging, we have to briefly talk about the TDSR (Total Debt Servicing Ratio) ruling. TDSR was introduced in 2013 by the government to prevent Singaporeans from excessive borrowing or over-leverage

In short, TDSR limits your monthly debt repayments to 60% of your gross income. For example, If you were to earn $1,000 per month, the maximum amount that you should use to service all your loans, which include housing debt, credit card loans, personal loans etc, is up to $600 per month.

TDSR is a permanent reform and stay around for the long term, unlike temporary cooling measures like ABSD (Additional Buyer Stamp Duty). The table below is the formula to calculate TDSR, not more than 60%.

After TDSR was introduced. There’s a very interesting phenomenon. We realized that more Singaporeans are willing to report a higher tax amount in order to take a higher loan.

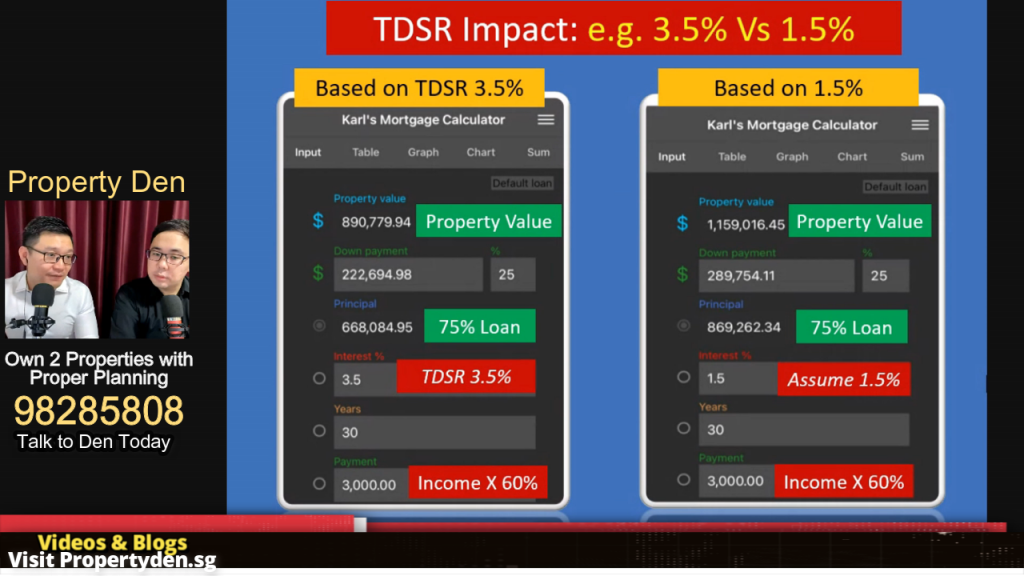

Let’s use an example to describe how does this 3.5% impact the amount of loan we can take. Both scenarios are based on the income of $5,000 and loan tenure of 30 years. On the left-hand side, that is where the TDSR is applied using 3.5%, if you work it backward, the property they can buy is $890k.

On the right, the calculations are based on the average loan interest rate of one by 1.5%. You can see the loan and the property value has increased substantially. In fact, the market interest rate now is about 1%, which is below our hypothetical 1.5%

If you look at the base of TDSR formula, a self employed or variable income earner who makes $9,000 per month, his income will be subjected to a 30% cut. When this individual fails the TDSR (71.5% > 60% Threshold) he will not be allowed to take the loan that he needs.

📌 Pledging or Show cash methods

When the bank tells you that your income is not enough to take the loan you desire, what can you do? This is a very common question.

One of the ways to increase your loan will be using the pledging and unpledging methods. There are many different terms for pledging and show-cash. In the market, pledging is also known as asset-based lending, while unpledging is also known as show cash or show fund. It’s all the same thing.

Basically, pledging literally means you pledge with the bank for 4 years and the bank will then in return give you a higher loan based on the assets that you have pledged with them

Show cash or show fund is different in the sense that you just need to show the bank two times. one during the loan application, then the second time is just before the loan is disbursed. For show cash, you do not need to lock down your funds and you only show it to the bank for a short period of time (7 days). It’s more flexible, but because it’s flexible, this amount will be larger than the pledging amount needed.

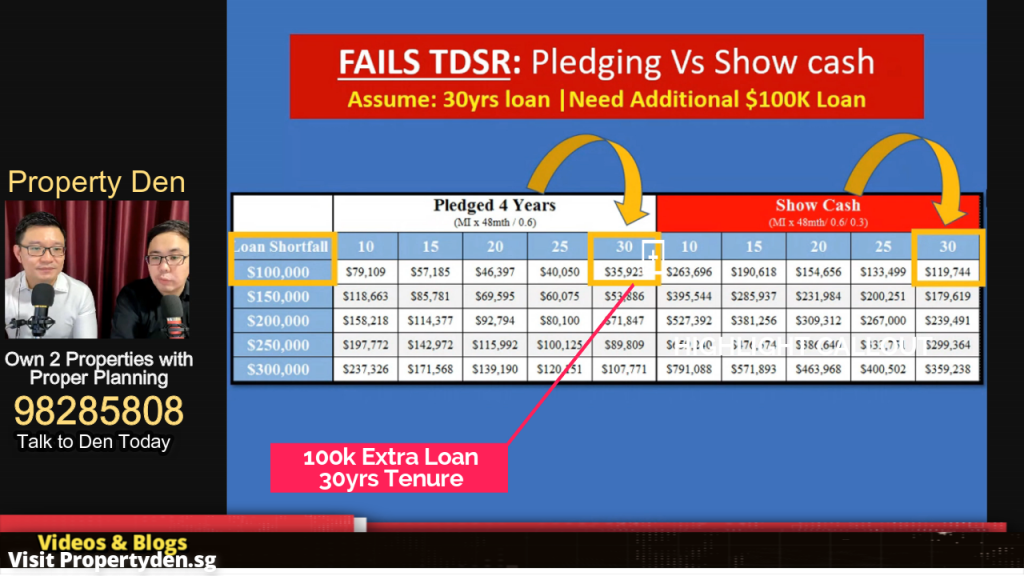

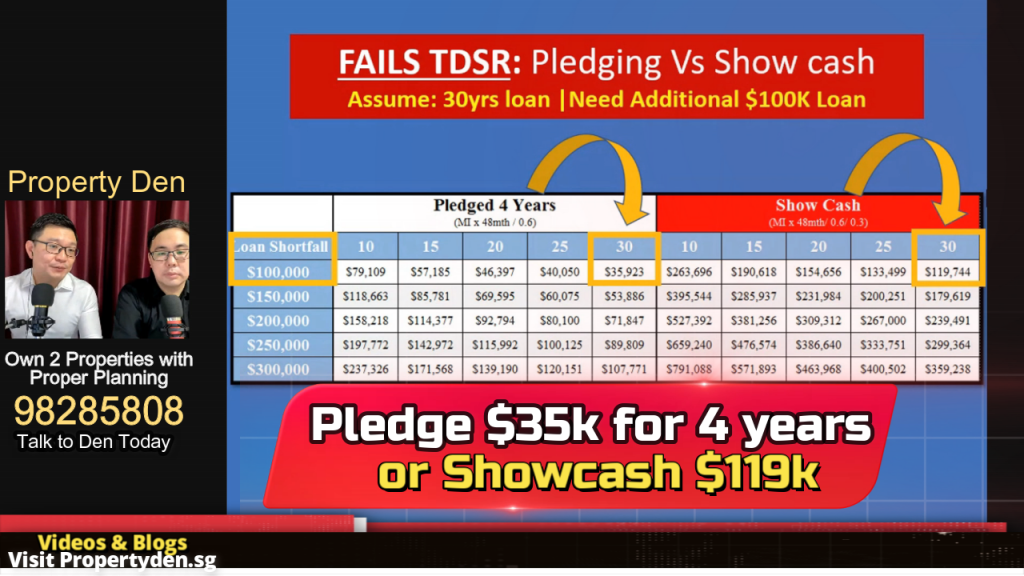

This table over here shows the loan shortfall and its corresponding pledging or show cash amount required. It might seem a bit intimidating for first timers who see this table. Let me try my best to explain this table in simple layman’s terms for you. Assuming a 30 years loan tenure, and you need an additional $100,000 loan

For the pledging method, you will need to put up with the bank $35K for four years, if your loan shortfall is $100k. For Show cash method, the amount will be higher at $119k

Note that all these numbers might differ a bit because of the rounding up calculations. Call us to give you the exact numbers. I you’re confused, just give us a call, we will do this breakdown for you.

Pledging is not the preferred method because most of our buyers prefer the short cash method because you don’t actually need to keep with the bank any assets for the next four years

📌 Summary

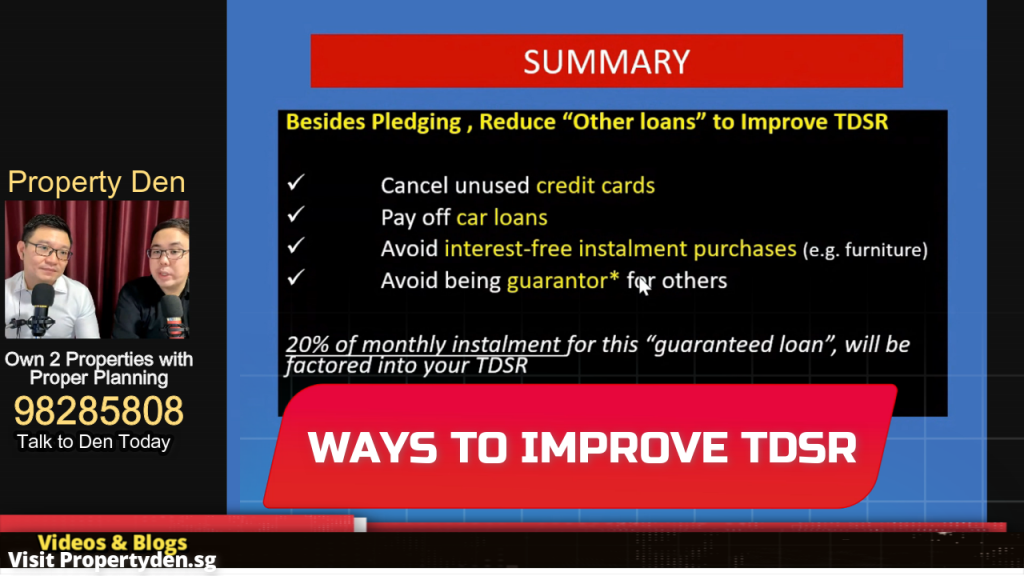

If you want to take a bigger loan, you either increase your fixed or variable income or reduce your liability. Beside pledging and show cash methods, there are other ways to improve your TDSR ratio. For example,

- If you have an unused credit card, please cancel it. For every credit card that you own, it will affect your TDSR ratio even if the card is not used or do not have any outstanding debt. This will reduce your eventual loan amount

- Pay off your car loans if possible

- Avoid interest-free instalment purchases for appliances or furniture from mega stores. A lot of people are also not aware these will impact your TDSR ratio

- Lastly, avoid being a guarantor for other people. To be more exact. If you’re guarantor for certain loan. 20% of this monthly instalment for this guaranteed loan will be factored into your TDSR, which means you can only take a lesser loan because of this guarantor role.

These are all the ways you can improve TDSR.

If you’re unsure of anything and feel like you need further assistance, feel free to give us a call. We’ll be more than happy to help you guys. we look forward to seeing you in the next video.

this video, we are going to share with you how to take a bigger loan, using the Pledging or Show-Cash method in order to buy your dream home.

Before we talk about pledging, we have to briefly talk about the TDSR (Total Debt Servicing Ratio) ruling. TDSR was introduced in 2013 by the government to prevent Singaporeans from excessive borrowing or over-leverage

In short, TDSR limits your monthly debt repayments to 60% of your gross income. For example, If you were to earn $1,000 per month, the maximum amount that you should use to service all your loans, which include housing debt, credit card loans, personal loans etcm, is up to $600 per month.

TDSR is a permanent reform and stay around for the long term, unlike temporary cooling measures like ABSD (Additional Buyer Stamp Duty). The table below is the formula to calculate TDSR, not more than 60%

Like this Article or Video?

Check out more Condo Tips here

Looking for new investment properties?

Talk to our experts from Homeseller to get more insights regarding the cash flow and capital gain of your property investments!

Insight Topics

Connect With Us

Recent

Investor Insights

Condo Buying Guide: How to Choose the Right Condo?

Condo Buying Guide! We’ll discuss various scenarios and provide expert recommendations based on factors like Property Type, Ownership Duration, Quantum

Read More

Does it have to be Freehold?

“Does it have to be freehold?” This is a common question buyers frequently ask. Find out the answer from Dennis & his team from Property Den.

Read More

When is Leasehold 99 Better than Freehold?

Freehold is always perceived to be better than Leasehold 99. So, when is leasehold 99 better than freehold? Find out more at Property Den.

Read More

Worst Mistake When Buying Condo

What is the worst mistake when buying a condo? Avoid making this costly mistake by checking out this article when buying for investment.

Read More

How to Select the Best Condo Unit | Avoid Low Floor?

Planning to buy a condo? how to select the best condo unit? Should you avoid low floor and units with no views? Is 1 bedroom or 2 bedroom better?

Read MoreTestimonials

"Dennis came with strong recommendations from a dear friend. He helped me with the purchase of my first property. He was very patient and never once tried to hard sell me to buy a property. Dennis is a trustworthy and knowledgeable professional who I highly recommend with confidence to everyone I know!"

HaoTing

Buyer

"Dennis was very helpful and has guided us throughout on the process. He managed to get good number of clients for viewing of our unit. He is very responsive and always readily available when needed. He has excellent negotiation skills as well when required for the deal"